Form 2290 Partial Period Tax Tables: Calculate HVUT for Short Tax Periods

Form 2290 Partial Period Tax Tables are the IRS proration charts used to figure Heavy Vehicle Use Tax (HVUT) when your truck is only taxable for part of the HVUT year. They let you pay only for the months your vehicle is first used on public highways, instead of a full 12 months.

Most “short tax period” situations happen when you buy a truck mid-year, put a seasonal unit back into service, or register a newly acquired vehicle. In this guide, you will learn how the IRS proration logic works, how to read the partial period tables (by weight and month), and how to turn those tables into clean, audit-friendly calculations. You will also see real-world planning takeaways that help owner-operators and fleet managers time filings, protect cash flow, and avoid registration delays.

What counts as a “partial period” for Form 2290?

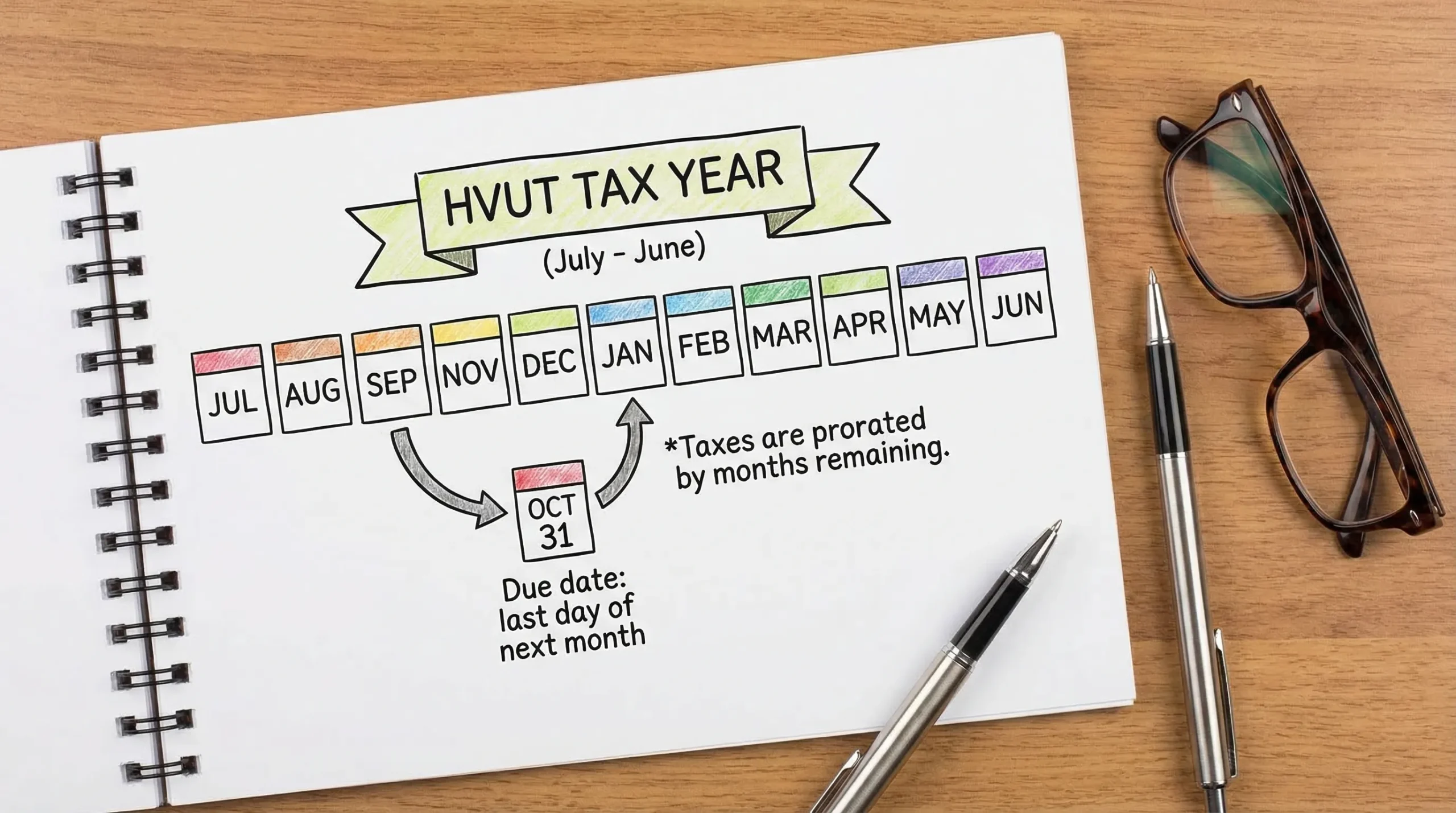

The HVUT tax year runs July 1 through June 30. If your vehicle is first used on public highways after July, you generally do not owe the full annual amount. Instead, you use the Form 2290 Partial Period Tax Tables (found in the IRS Form 2290 instructions) to determine the prorated amount based on your First Used Month (FUM).

Common triggers for a short tax period include:

- You purchased (or leased) a vehicle and first used it on public highways mid-year.

- A vehicle that was previously out of service becomes operational and first used again during the tax year.

- You are registering under IRP and need a current Schedule 1 quickly for plates (see irp truck registration).

Authoritative reference: the IRS explains proration and provides the tables in the official Form 2290 Instructions.

The IRS proration rule in one simple formula

Even if you plan to use the IRS 2290 partial period tax table, it helps to understand what it is doing:

Prorated HVUT = Annual HVUT amount × (Months remaining in the HVUT year starting with FUM) ÷ 12

The tables simply pre-calculate those prorated amounts for each taxable gross weight category.

Months remaining cheat sheet (based on first used month)

Here is the core logic behind every HVUT partial period tax table:

| First used month | Months taxable (through June 30) | Fraction of annual tax |

|---|---|---|

| July | 12 | 12/12 |

| August | 11 | 11/12 |

| September | 10 | 10/12 |

| October | 9 | 9/12 |

| November | 8 | 8/12 |

| December | 7 | 7/12 |

| January | 6 | 6/12 |

| February | 5 | 5/12 |

| March | 4 | 4/12 |

| April | 3 | 3/12 |

| May | 2 | 2/12 |

| June | 1 | 1/12 |

This is also why IRS filing dates matter operationally: your Form 2290 is due by the last day of the month after your first used month, and registration workflows often depend on having your stamped Schedule 1 on time (see schedule 1 form 2290 due).

How to read the Form 2290 partial period tables (without overpaying)

The Form 2290 Partial Period Tax Tables work like a grid:

- One dimension is your taxable gross weight category (A through V), which comes from your taxable gross weight category.

- The other dimension is your first used month.

Your job is to pick the correct weight bracket and month, then read the tax amount at the intersection.

A few important details that drive the number you see:

- The IRS heavy vehicle use tax table has different rates for taxable (regular) vehicles versus qualified logging vehicles.

- Vehicles over 75,000 lbs hit the maximum annual HVUT for regular vehicles (commonly shown as $550), and the partial-period table prorates down from that maximum.

- Suspended (low-mileage) vehicles are handled differently (Category W). They may still require filing even if no tax is due.

If you want the deeper “why” behind the numbers and weight tiers, use this companion guide: HVUT tax rates by weight.

Worked examples: prorated HVUT using the partial period tables

Below are “show your work” examples you can keep in your records. These align with how the 2290 tax calculation table is structured.

Example 1: Over 75,000 lbs (max-rate truck) first used in January

- Vehicle: Regular (non-logging)

- Weight: Over 75,000 lbs (max annual rate group)

- First used month: January

Months taxable from January to June = 6 months.

If your annual HVUT at this weight is $550, the prorated tax is:

$550 × (6/12) = $275

In the Form 2290 Partial Period Tax Tables, you should see the January amount for that max-rate category align with this proration.

Example 2: 60,000 lbs first used in March (classic mid-year purchase)

For many 55,000 to 75,000 lb vehicles, the annual tax is computed based on weight increments. A common reference point is that a 60,000 lb truck’s annual HVUT is often shown as $210 (based on IRS rate structure).

- Annual HVUT amount (example): $210

- First used month: March

- Months taxable March to June = 4 months

Prorated tax:

$210 × (4/12) = $70

Your form 2290 prorated tax table lookup for that weight bracket and March should land at the same figure.

Example 3: Fleet filing reality check (why small errors get expensive)

Assume a small fleet “invests” in 10 used tractors late in the year to expand a new lane. Each tractor falls into the max-rate category.

- If first used in July: $550 × 10 = $5,500

- If first used in January: $275 × 10 = $2,750

That is a $2,750 cash flow swing driven purely by timing of first use and correct month selection in the Form 2290 Partial Period Tax Tables.

A quick planning table: cash impact for max-rate vehicles

This is not an IRS table, it is a decision table based on proration math that helps with budgeting.

| First used month | Months taxable | Estimated HVUT due if annual is $550 |

|---|---|---|

| July | 12 | $550.00 |

| October | 9 | $412.50 |

| January | 6 | $275.00 |

| April | 3 | $137.50 |

| June | 1 | $45.83 |

Strategic takeaway: for seasonal operations and late-year expansions, aligning operational “first use” with reality (and documenting it) is a meaningful lever for working capital.

Where fleets lose time (and get rejected): lessons learned

The IRS tables are straightforward, but rejection risk and registration delays typically come from input errors rather than the math.

The highest-impact checks to build into your process:

- First used month vs. purchase date: the FUM is when the vehicle is first used on public highways in the period, not the invoice date.

- VIN accuracy: a single digit error can block acceptance and delay plates. Keep your vehicle identification number source document handy.

- Weight changes: if your taxable gross weight increases later, that is usually handled via an amendment, not by changing your original month. See Taxable Weight Amendments.

Also note an operational rule that becomes a “trend” as fleets scale: the IRS generally requires e-filing when reporting many vehicles. The IRS instructions explain when electronic filing is mandatory, and in practice, that pushes growing carriers toward standardized workflows.

Why e-filing matters for partial-period filings

Short-period filings are often time-sensitive because you need proof quickly. E-filing through an IRS Authorized E-file Provider can reduce friction because the system validates key fields and produces proof faster than paper.

With Simple Form 2290, you can complete an online guided process, handle multi-vehicle filings, and receive your Form 2290 schedule 1 after IRS acceptance. For fleets, tools that support Bulk and fleet filing are especially helpful when multiple vehicles have different first used months.

Frequently Asked Questions

What are Form 2290 Partial Period Tax Tables used for? They are used to calculate prorated HVUT when a truck is first used on public highways after July, so you pay only for the remaining months in the HVUT tax year.

Where do I find the IRS 2290 partial period tax table? The IRS publishes the IRS 2290 partial period tax table in the official Form 2290 instructions on IRS.gov.

How do I calculate HVUT using the HVUT partial period tax table? Find your taxable gross weight category, then locate your first used month in the table. The intersection shows the prorated tax for that short period.

Is the form 2290 prorated tax table the same as a credit for selling a truck? Not exactly. The proration table calculates tax owed from the first used month through June 30. Credits for sold, stolen, or destroyed vehicles are claimed separately using IRS rules and forms.

What if I enter the wrong first used month or weight category? You may overpay, underpay, or get rejected. If your weight increases later, you typically file an amendment (see taxable weight increase guidance) and keep documentation supporting your first used month.

File the right prorated amount and get Schedule 1 fast

If you are using Form 2290 Partial Period Tax Tables because you added a truck mid-year, timing matters. The faster you file correctly, the faster you can get proof for registration and keep the truck earning.

File online with Simple Form 2290 to streamline your HVUT prorated tax calculation, reduce errors, and receive your stamped Schedule 1 after IRS acceptance. Start here: electronic file form 2290 and pay online.